http://seekingalpha.com/article/3969480-nevsun-resources-bisha-mine-cash-flow-strong-acquisition

Nevsun Resources: Bisha Mine Cash Flow And A Strong Acquisition

Apr. 29, 2016 8:13 AM ET| About: Nevsun Resources Ltd. (NSU), Includes: FCX

The Value Portfolio

Growth, long-term horizon, deep value, momentum

Summary

-Nevsun Resources has seen its stock prices drop from the commodity highs of 2011 that saw stock prices at almost $7.

-At the same time, the company's exploration plan has been significantly accretive to it and has helped its growth.

-I recommend investors open positions in the company or invest at present prices.

Introduction

Nevsun Resources (NYSEMKT: NSU) is a Canadian mining company that operates the Bisha mine in Eritrea, Africa. The mine is a joint venture with the Eritrean government with Nevsun Resources owning 60% and the government owning the other 40%. The mine has a reserve life of more than a decade that is constantly being expanded, and offers a dividend yield of almost 5%.

Nevsun Resources Bisha Mine - Asmarino

For a company with only a single asset, the Bisha Mine is a good one to have. The mine is a massive VMS (volcanogenic massive sulfide ore deposit) with millions of metric tons of ore amounting to billions of dollars of metals such as copper, gold, zinc, and silver.

Operations

Now it is time to talk about the company's operations.

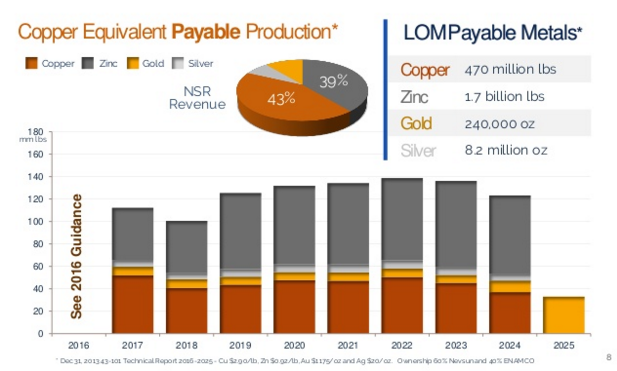

https://staticseekingalpha.a.ssl.fastly.net/uploads/2016/4/25/saupload_E00l-VmBTPCRNe52J9EYh-t1o1fsluG6uMdtrNSOCL7OU2-zcrrueDR_fDHzBrzD7ynI0UQ-bNN9xlUTPZCQ2BHZHcXQWIQc16kx_Xb70KbmuVVf_7wKzlQFIT6vMAwRhK8b8rq9.png

Nevsun Resources Payable Production - Nevsun Resources Investor Presentation

The above image shows Nevsun Resources' mining plan up until the end of the Bisha Mine reserves in 2025. The company's production consists of copper, zinc, gold, and silver with the mine having 1.1 billion pounds of payable copper equivalent. The company's copper costs have been approximately $1.3 per pound and copper prices are hovering at around $2.

In recent weeks, copper prices have been going up and are currently hovering at almost $2.3 per pound. That means for every pound of copper the company produces, it makes $1 of profit. With 30 million pounds of copper production annually, that's $30 million in annual pure profits from just copper.

At the same time, the company plans on turning increasingly to zinc production with its zinc processing plant which is expected to turn on this year. Silver and gold will provide a nice additional profitable base with the company having $280 million of gold and $140 million of silver providing revenues. Assuming the company maintains a 40% profit ratio, that's another $170 million of profits over the coming decade.

Nevsun Resources Proven and Probable Pit Resources - Nevsun Resources Investor Presentation

An overview of where these reserves come from is provided above. The mine consists of 870 kilotons of supergene ore which has almost been mined through and another 21,000 kilotons of ore which are yet to be mined. These reserves, while they do have lower copper rates, do have respectable zinc rates with higher gold and noticeably higher silver rates.

However, it is worth paying attention to one key potential negative with that 1.10% copper number. That copper number is based on feasibility explorations at $2.74/pound copper prices. Prices have held themselves 10-20% below that in recent months and that points towards lower reserves that what is actually feasible.

However, higher gold prices point towards additional revenue.

What matters though is not what potential the mine has but instead what potential the company is taking advantage of.

Nevsun Resources Production 2016 - Nevsun Resources Investor Presentation

The first phase of the company's expansion project for the coming years is its zinc plant. The company has 2.6 billion pounds of zinc in reserves along with another 3.5 billion pounds of zinc contained in resources. That is 6.1 billion pounds of zinc with a market value of $5.2 billion at current prices.

Again assuming a 40% profit rate, or even a much smaller 15% profit rate that is more profits over the coming years to decade than the company's entire market cap. To achieve the processing of this ore, the company created an $80 million zinc flotation and storage plant which is one of the few major corporate projects I have seen come in both on-time and under budget.

At the same time, beyond the company's zinc production phase, the company is also working on additional aggressive exploration.

Nevsun Resources Districts - Nevsun Resources Investor Presentation

The company has three major exploration districts with the Bisha District representing the company's current main one having 40 Mt of resources. The Flin Flon District and Noranda District together have more than 400 Mt of additional resources or more than 10 times what the Bisha district has.

Assuming they have 10 times the resource, this could easily make Nevsun Resources a ten-bagger or more. That would make Nevsun Resources a multi-billion dollar mining company, placing it in league with the largest mining companies in the world and all this from the company's single mine. More so, this cash cow will enable the company to make additional accretive acquisitions.

Nevsun Resources 2016 Exploration Plan - Nevsun Resources Investor Presentation

The company's 2016 exploration plan has an $11 million budget, which, if history is any indicator, should be significantly accretive to the company's resources and reserve life. This exploration plan includes 34 km of exploratory drilling with the despots (gray) extending significantly out of the current resources highlighted in gold.

Nevsun Resources Harena Drilling Results - Nevsun Resources Investor Presentation

The potential of the 2016 drilling plan can be seen in the company's 2015 drilling results as evidenced by the Harena extension drilling program which operated throughout 2015. The two main regions of exploration were the HX-069 and the HX-071 plans which have 5.0-10.2% zinc. However, these plans do have relatively minimal gold and silver resources with relatively low copper resources which may not be profitable.

Reservoir Minerals Acquisition

Now that we have talked about the company's operations, it is now time to talk about the company's recent reservoir minerals acquisition.

Reservoir Minerals - Mining Scout

One of the major complaints investors have had with Nevsun Resources is the company's impressive cash pile. The company has a $600 million market cap and a cash pile that makes up 2/3 of that. That places the company's enterprise value at $200 million. Let us now assume for a moment that the company made a special dividend of the $400 million cash pile or $2.2 per share.

That means the leftover company with a $200 million enterprise value will still be making $30 million a year in profits or $0.14 per share. That is a P/E value of 8 compared to the new share price of $1.1 after the dividend. However, the company's current $0.14 profits give it a present P/E ratio of ~24. This presents a significantly better-valued company in the opinion of most shareholders.

However, the company recently agreed to acquire Reservoir Minerals (OTCPK:RVRLF) for a combination of $365 million in cash and stock. Nevsun Resources will give (2) shares to Reservoir Minerals for each share of the stock while also providing $135 million in financing for the company.

Personally, I am disappointed by the company's acquisition of the company using primarily stock. That means even subtracting the company's $135 million cash pile, it still holds hundreds of millions of cash that isn't being applied to anything. While this cash could be used to help Reservoir Minerals with its high potential projects, that usage will likely last a decade or more.

However, the financing does allow Reservoir Mineral to exercise a right with Freeport-McMoRan (NYSE: FCX) giving the company 100% of Timok's Upper Zone and 60.4% of the Lower Zone.

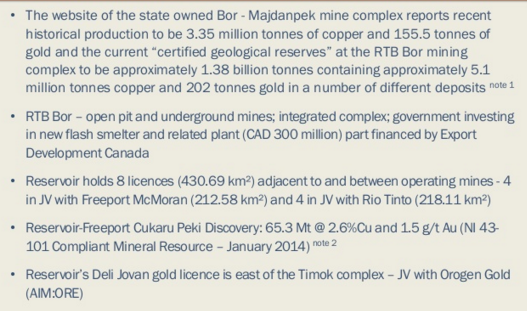

https://staticseekingalpha.a.ssl.fastly.net/uploads/2016/4/26/34591885-14616850829286687.png

Reservoir Acquisition - Nevsun PR Release

The above image provides an overview of the exploration at the Timok project. Reservoir holds 8 licenses amounting to 430.69 square kilometers of land split among a JV with Freeport-McMoRan and Rio Tinto (NYSE:RIO) both major mining companies with an impressive history of exploration.

However, what is most important in the above document is the fourth line - the company's Cukaru Peki discovery. Here, the company found 65.3 Mt _at_ 2.6% copper and 1.5g/t both economical values for mining. The value of these resources, assuming they are fully extractable is $8 billion of copper along with $4 billion of gold.

Current exploration shows the Timok Project holds billions of dollars of copper and other metals. This mine will likely start up in the next half a decade or more and will have a multi-decade reserve life bringing hundreds of millions per year. This mine will provide Nevsun Resources with a multi-decade reserve life that will allow it to continue its process of paying a significant dividend to investors.

My Take

Nevsun Resources is one of the few major mines that continues earning money. The company is a cash cow with an impressive cash pile. This cash pile allows the company to give both a respectable dividend yield and potentially acquire more expensive assets.

At the same time, the company has a long and impressive exploration history with another $11 million slated for exploration in 2016. The 2015 exploration yielded impressive zinc concentration in the money with limited findings of other metals. Still these explorations will likely be highly profitable and accretive to the company's earnings.

I see Nevsun Resources as a low-risk cash cow for interested investors. The company's significant cash pile limits the downside risk while the company already has proven resources that can be mined. More so, the company's 40% profit margin at current commodity prices minimizes the chances of the company becoming unprofitable. In fact, most expect commodity prices to rise from their present levels.

Conclusion

Nevsun Resources has had a difficult time recently with the company's stock price taking a significant hit from prices of almost $7 in 2011. However, the company has maintained a steady price recently and offers a very respectable dividend yield of almost 5%.

At the same time, the company has been able to undertake a very accretive exploration project. That means that while the mine has been running for half a decade, its reserve life has not actually changed. Continued exploration expected to cost the company $11 million for 2016 coupled with the startup of the zinc processing plant will increase the company's income.

As a result, I recommend investors use current prices or any drops as a chance to increase their stake significantly.

Received on Fri Apr 29 2016 - 12:49:32 EDT

{kind=link}

{kind=link}