03 The economic value of sesame and its role as a transnational ‘conflict commodity’

Sesame is a valuable cash crop in Ethiopia and Sudan. Since 2020, the areas in which some of the best-quality sesame is cultivated have suffered conflict and instability. The crop has thus become a strategic commodity, the proceeds of which have been used to sustain conflict.

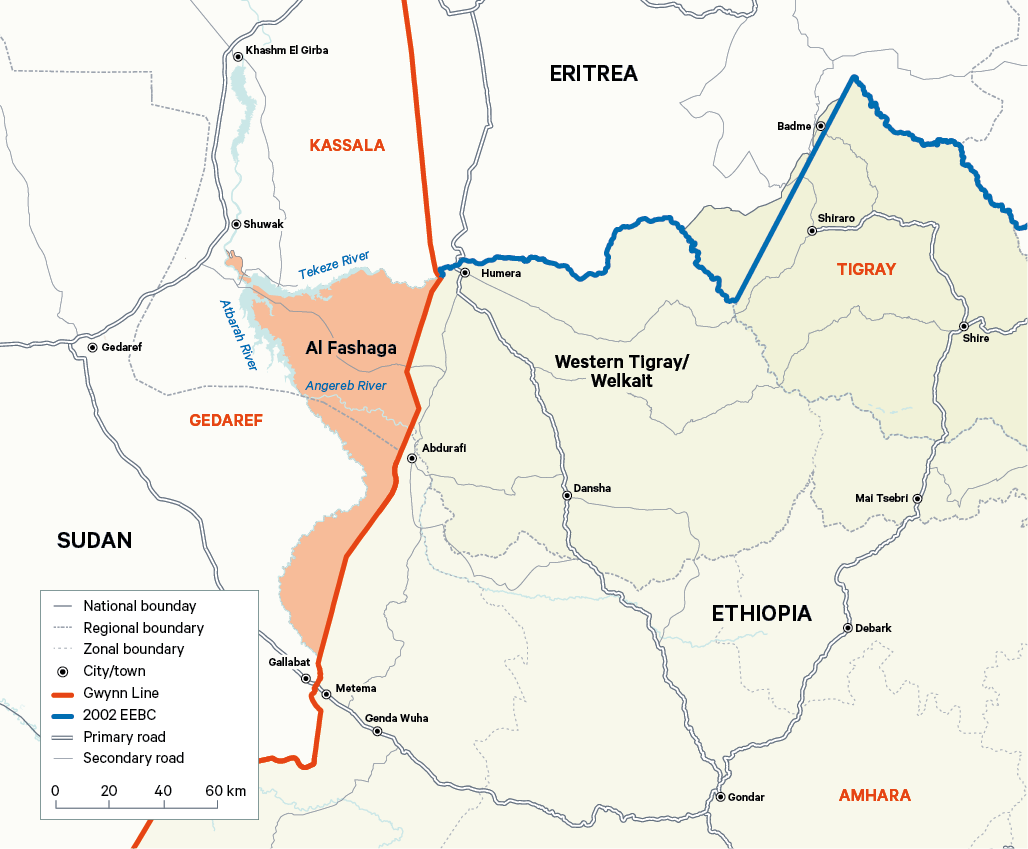

Sesame is the world’s oldest oilseed crop, originating from East Africa and Asia. It has historically been an important export crop for the predominantly agrarian economies of Sudan and Ethiopia. One of the key areas of sesame production (see Figure 1) is on either side of the border between the two countries, encompassing the eastern Sudanese states of Gedaref and Kassala, and the Amhara and Tigray regional states of northwestern Ethiopia.25 Sandwiched between them lies the disputed area of Al Fashaga.

Figure 1. Map of Ethiopia–Sudan border

The global sesame seed market was estimated to be worth $7.5 billion in 2023 and is expected to grow to $8.5 billion by 2028.26 The demand for sesame is largely due to its nutritious properties and its inclusion in a variety of foods.27 Ethiopia and Sudan have both ranked among the top 10 producers and exporters of the crop over the last decade.28 The type of white sesame produced in Gedaref and Humera, known as ‘white gold’ due to its colour, is in high demand. This is a function of both its quality and the relatively limited area in which it is produced. The crop is politically important, as the value chain has historically been controlled by local elites. Before the escalation of the dispute over Al Fashaga in December 2020, Ethiopian and Sudanese farmers had sold their sesame products in both countries, with the dynamics of this trade largely being determined by market conditions and structures, such as pricing and the profit margins sought by investors, traders and farmers.

The sesame industry in Ethiopia

The oilseed industry has been a major contributor to Ethiopia’s foreign exchange revenues in recent years, providing between $250 million and $500 million in export earnings per year over the last decade. The three main oilseed crops – sesame, soybean and niger seeds – contribute one-fifth of Ethiopia’s agricultural export profits,29 with the majority of this share coming from sesame. Oilseed farming of one kind or another provides a living for more than 3.7 million smallholders.30

Most of Ethiopia’s commercial sesame production has historically occurred in its northern and northwestern regions – notably in the Welkait, Metema and Humera woredas,31 close to the borders with Sudan and Eritrea.32 Until recently, Amhara regional state contributed 44 per cent of national sesame exports, while neighbouring Tigray contributed 31 per cent and Oromia 13 per cent. Sesame is also farmed on a smaller scale in several other regional states of Ethiopia.33

The sesame industry has been severely affected by conflict. Humera and Welkait were part of Western Tigray until they were annexed by Amhara forces in late 2020. Wollega in Western Oromia is also insecure, as the rebel Oromo Liberation Army has been conducting an insurgency in this area. The impact of conflict on production is indicated by figures showing that between 2019 and 2021, the total area in which sesame was harvested in Ethiopia declined from 375,120 ha to 270,000 ha.34 Additionally, actual exports of sesame more than halved between 2020 and 2022, from 247,501 metric tons to 107,719 metric tons.35 Yet, somewhat surprisingly, the country’s producers did not revise their export predictions as a result: in late 2022 (when the most recent forecasts were published), they still envisaged exporting 230,000 metric tons of sesame in 2023.36

The sesame industry in Sudan

Agricultural exports have become even more vital to Sudan’s economy since 2011, after the secession of South Sudan drastically reduced earnings from the petroleum sector. Sesame is one of Sudan’s main agricultural exports in the post-oil era: between 2011 and 2021, sesame accounted for nearly 30 per cent of such exports (inclusive of crops and livestock).37 Moreover, the area of sesame harvested in Sudan increased from 2.16 million ha in 2013 to over 4.15 million ha in 2022.38

Nearly 80 per cent of the area devoted to sesame seed farming is in the states of Gedaref, North Kordofan and Blue Nile, with the Darfuri states also contributing a significant share of production.39 All these regions were marginalized during more than 30 years of rule by the NCP. Darfur, Kordofan and Blue Nile have also been significantly affected by the current war. Mass violence and displacement in the five states of Darfur have decimated farming and subsistence livelihoods, while in North Kordofan supply lines and trading markets have been impacted by the RSF’s southern advance. The Sudan People’s Liberation Movement-North (SPLM-N), led by Abdul Aziz al-Hilu, has sought to consolidate its control in South Kordofan, including over agricultural areas. The SPLM-N has also fought the SAF and allied forces in neighbouring Blue Nile state.

Nearly 80 per cent of the area devoted to sesame seed farming is in the states of Gedaref, North Kordofan and Blue Nile, with the Darfuri states also contributing a significant share of production.

Gedaref, still under the control of the national army (i.e. the SAF), has remained relatively stable in comparison. The state is considered to be part of Sudan’s ‘breadbasket’. It is well known for producing premium-quality sesame, contributing 30 per cent of Sudan’s production.40

Roughly one-half of national sesame production is semi-mechanized, while the other half comes from the traditional rain-fed sector.41 Production of high-grade white sesame tends to be semi-mechanized, taking place largely on commercial farms leased by well-connected traders and security officials. Such farms are often oriented towards profit-making rather than serving the long-term development and interests of local communities.42

Many of the workers on Gedaref’s sesame farms are migrants who have made arduous journeys to reach the area, and who then endure harsh working conditions. Large-scale farmers in Sudan source labour through both legal and illegal channels, and recruit tens of thousands of Ethiopian seasonal migrant workers for the planting and harvesting periods.43 Workers are poorly paid and vulnerable to abuse as ‘increased production involves further over-exploitation of both land and labour’.44 Labour exploitation is further fuelled by the persistence of historic power inequalities between the centre of the country and the geographic margins of Sudan. Members of the central elites – including some government officials, security officers and businesspeople – often demonstrate predatory approaches to land and resource use, and to dealings with people, in rural areas. This has resulted in recurring cycles of impoverishment and violence.

Sesame’s role as a transnational conflict good

Production of sesame and revenues from its trade have fluctuated in Ethiopia and Sudan in recent years, in part due to the tumultuous political and security contexts in both countries. Ethiopia’s revenues from sesame exports totalled $282 million in 2018. Subsequent revenues were uneven, but totalled $182 million in 2022 (the most recent year for which data are available).45 The value of Sudanese sesame exports earnings rose from $576 million in 2018 to a peak of $789 million in 2020 before falling to $488 million in 2022.46 Despite this, sesame remains one of Sudan’s most valuable export commodities after gold, roughly on a par with livestock.47

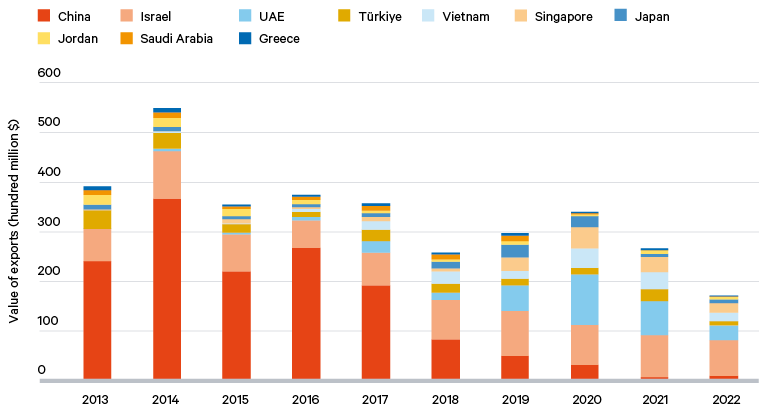

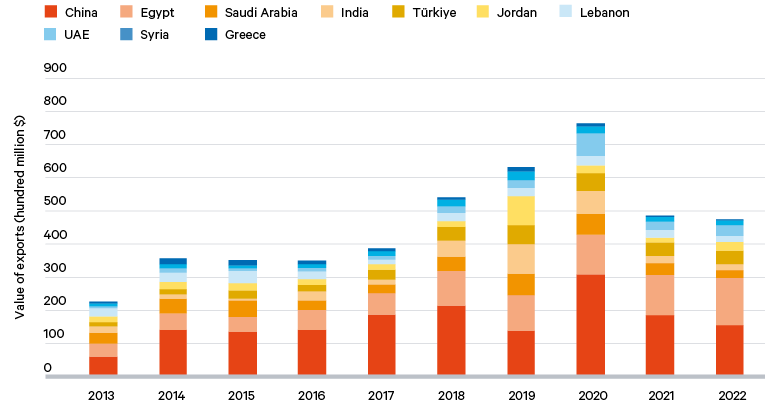

Figures 2 and 3 respectively illustrate Ethiopia and Sudan’s top sesame seed export markets over the past decade.

Figure 2. Ethiopia’s top sesame seed export markets48

Figure 3. Sudan’s top sesame seed export markets49

These data suggest a correlation between transnational relations and trade. Some of the largest importers of Ethiopian and Sudanese sesame are also among the countries that have played an outsized role in shaping the region’s tumultuous political shifts in recent years.

For Ethiopia, the most important sesame export markets have included Israel, the UAE and, until recently, China. Of these partners, the UAE is an important supporter of the Ethiopian federal government, having invested to aid the struggling Ethiopian economy as well as having delivered critical military supplies to help turn the tide of the Tigray war.50

Of Sudan’s main sesame export markets, Egypt, Saudi Arabia and the UAE warrant particular attention in terms of the intersection between their trade relations and diplomatic agendas. These countries are leading regional stakeholders with direct interests in shaping the outcome of the war in Sudan. Egypt maintains strong relations with the SAF and has close economic links with Sudan more widely, particularly in agriculture. The Saudis, meanwhile, have been closely involved in mediation between the warring parties. The UAE – a key backer of the RSF – was also a significant importer of Sudanese sesame before the conflict started. Saudi and Emirati interests in Ethiopia and Sudan are partly shaped by their aspirations to boost their own food security.

Türkiye is another important destination for Sudanese sesame. Both Ethiopia’s government and the SAF have sought to procure Turkish-made drones during their internal conflicts,51 with the Sudanese military regime also seeking economic support from its regional allies through the sale of strategic commodities such as sesame, gold and livestock.

The data on Ethiopia and Sudan’s sesame exports highlights the link between diplomatic alliances and transnational trade, which also converge with conflict dynamics. There is a credible argument to be made that sesame, normally an agricultural crop without obvious military relevance, has become a securitized economic resource or ‘conflict commodity’. This reflects the fact that its production and trade have been captured and controlled by armed groups, and that the proceeds from such trade are used to fuel conflict by national or subnational actors. Thus, the definition of what constitutes a conflict good needs to be expanded beyond the products or commodities typically associated with armed violence – such as illicit minerals, weapons or drugs.52 The sesame industry not only connects Ethiopia and Sudan to other regional powers – notably, as mentioned, in the Middle East – but also fuels a war economy that sustains conflict in both countries. Moreover, given the large financial interests at stake, the new dynamics of such an economy can make the resolution of conflict more difficult.